Blog > Cx excellence

How to outsource your customer support as a payments platform

Payments is one of the few industries where exceptional customer support (and usually 24/7 support) is the expectation and standard.

Influx works with payments and fintech platforms to deliver always-on, high-accuracy support, providing both an AI layer and fully-managed outsourced teams.

As a payments platform, how do you outsource your support though? How much scope do you give to your outsourced team vs AI vs in-house?

This post answers that question using specific examples from Influx payments clients and presents a simple framework.

What to outsource, and what to keep in-house

A high-standard split for a well-structured team is 40% AI, 40% outsourcing, 20% in-house. That work breaks down as follows:

And then here’s examples for each category:

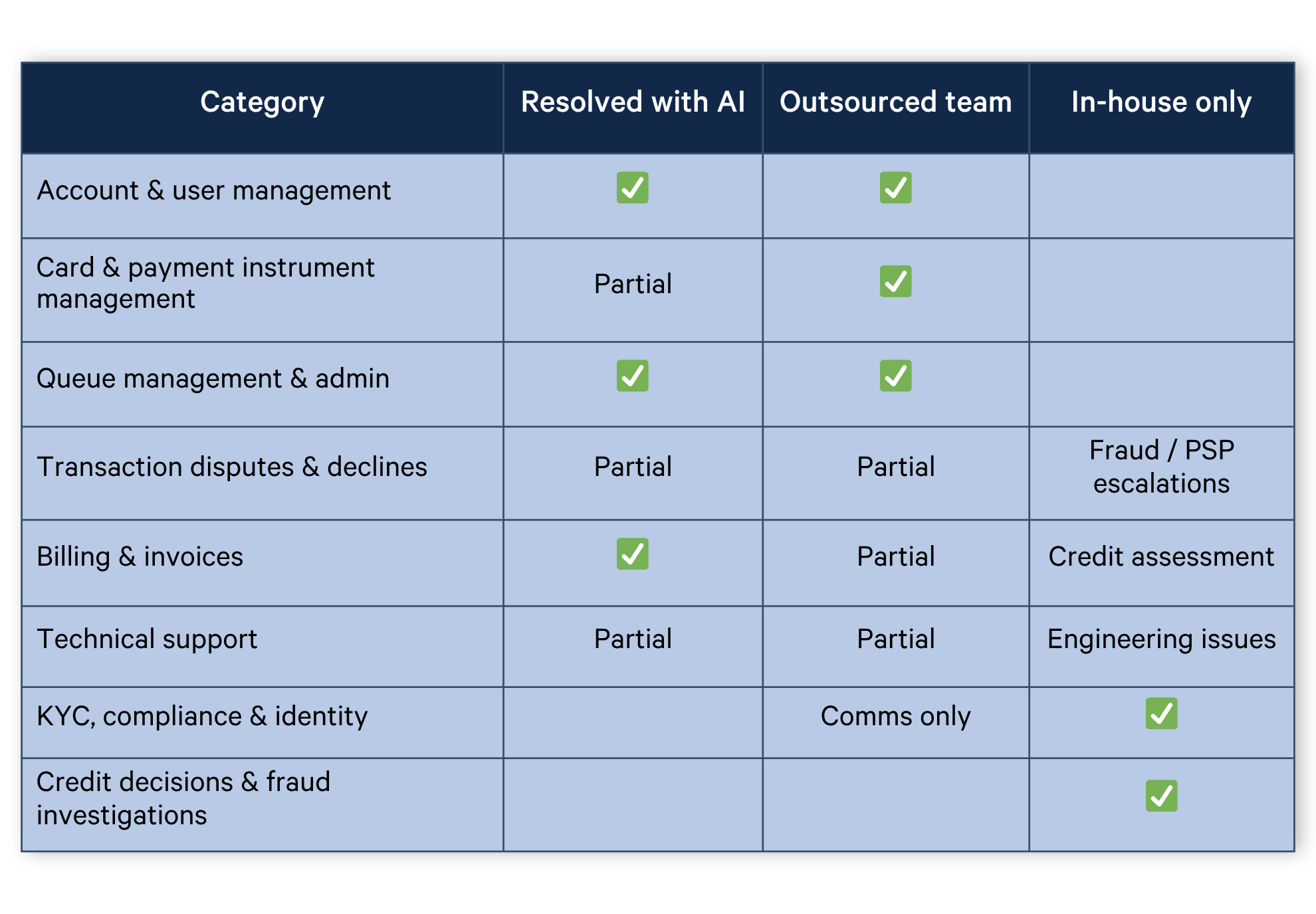

| Category | Sample message | What Influx.com handles |

|---|---|---|

| Account & user management | "I can't log in. Can you reset my password and add my colleague as a user?" | Portal access, password resets, user setup, contact and address changes. New accounts requiring credit approval stay in-house. |

| Card & payment instrument management | "My card was lost. I need a replacement sent to our depot and the old one cancelled." | Full card lifecycle: new cards, replacements, terminations, PIN resets, limit changes, gift card activation, and withdrawal management. Bulk reissues and partner-card products stay in-house. |

| Transaction disputes & declines | "My card was declined at the pump but I had enough credit. What happened?" | Standard L1 diagnosis: limit exceeded, invalid product, invalid PIN. Complex PSP disputes and fraud investigations escalate to your internal team. |

| Billing, invoices & payments | "Can you send my October invoice? I think I've been charged a late fee incorrectly." | Invoice copies, remittance processing, fee reversals within a defined authority level, and proof-of-payment collection. Credit assessments and payment cycle changes stay in-house. |

| Technical & platform support | "My accounting integration stopped syncing after I updated my account details." | Known issues with documented fixes: portal bugs, integration errors, bot-to-human handoff problems. Engineering-level bugs and platform migrations stay in-house. |

| Compliance, KYC & identity | "My account has been blocked. I submitted my documents two days ago and haven't heard back." | Authentication checks, KYC status communications, and account block explanations. KYC decisions, legal review, fraud-driven restrictions, and identity policy changes stay in-house. |

| Queue management & admin | Automated reports, duplicate tickets, bulk emails with no customer query. | Full ownership: queue grooming, duplicate merging, spam triage, case attribution, and internal routing. |

Outsource freely:

- Account and user management: password resets, portal access, contact updates. High volume, well-defined, zero judgment required.

- Card and payment instrument management: new cards, replacements, cancellations, PIN resets, limit changes.

- Queue management and admin: routing, merging duplicates, spam triage. Pure operational overhead that shouldn't touch your internal team.

Outsource with defined limits:

- Transaction disputes and declines: standard diagnosis (limit exceeded, wrong PIN, invalid product) is fully outsourceable. Cases that require escalating to a payment service provider or involve suspected fraud need a clear handoff to in-house.

- Billing and invoices: sending invoice copies, explaining fees, processing standard reversals within a defined authority level. Anything requiring credit assessment or financial authority above agent tier stays internal.

- Technical support: known issues with documented fixes are fair game. Anything requiring engineering is not.

Keep in-house:

- KYC, compliance, and identity decisions. An outsourced agent can explain that a document was received and set expectations on timeline. The decision itself (approve, reject, escalate) carries regulatory weight that needs to sit with your team.

- Credit decisions, fraud investigations, account terminations, and anything with legal exposure.The failure mode to avoid: giving external agents system access without the authority to use it. If every fee reversal needs internal sign-off, your outsourced team is an expensive message relay.

When managed effectively, here’s how work breaks down between teams (AI vs outsourcing vs in-house):

40%

by AI

40%

by Outsourced Team

20%

by Internal Team

How the best payments platforms outsource: Build a tiered model

L1 handles standard queries end-to-end. L2 handles escalations, or cases that need deeper investigation or back-office action. The tier boundaries are defined in writing, including what each tier can and can't action.

This prevents the two failure modes: agents escalating too early, creating bottlenecks; or agents attempting to resolve things they don't have the authority to close.

They use AI as a first pass, not a replacement. The best setups deploy a bot to handle FAQ deflection, routing, and basic status checks before a human gets involved. This works when the bot-to-human handoff is seamless and the agent receives full context. It breaks down when the bot contradicts what the agent says, or customers feel stuck in a loop.

They treat the outsourced team as a second delivery team. The platforms that get the most out of outsourcing embed their external team into Slack, shared QA frameworks, and calibration calls. They don't manage them at arm's length. The outsourced agents know the product, know the escalation paths, and know the difference between a pending status that resolves itself and one that needs a PSP call.

Operational rhythms that make it work

A good outsourcing relationship runs on consistent cadences, not ad hoc check-ins when something breaks.

Weekly: Review the prior week's metrics (FRT, AHT, CSAT, SLA), walk through a handful of DSAT cases together, and surface any new issue types generating volume. The qualitative review matters as much as the numbers.

Monthly: Trend analysis like volume patterns, QA movement, escalation rate changes, staffing utilisation. This is where structural decisions get made: adjusting scope, resizing the team, shifting KPIs.

Quarterly: Playbook review. Products change, regulations evolve, and documentation goes stale fast. A quarterly refresh, where the internal team updates the playbooks and the outsourced team flags where documentation doesn't match reality, keeps agents working from accurate information.

Define your incident response protocol before you need it. When a processor goes down or a fraud campaign hits, both teams need to know immediately who owns what.

How to onboard a new outsourcing partner

Documentation before access. The most common onboarding mistake is giving agents system access before they understand the product. Tool-first training produces agents who can navigate your helpdesk but have no mental model of what they're solving. Start with product knowledge, then layer in tooling.

Documentation needs to cover: scope of authority, case type taxonomy with real examples, escalation paths with named contacts, authentication procedures, and brand voice guidelines. For payments specifically, include guidance on how to communicate about blocked accounts, rejected KYC, and failed transactions in a way that's honest and empathetic without creating liability.

Run a drafting phase. For the first two to four weeks, have agents compose responses for internal review before sending. It surfaces knowledge gaps before they reach customers and calibrates the team quickly. Transition to live handling gradually: start with the simplest, highest-volume case types and expand scope as performance stabilises.

Map every escalation path before go-live. For every case type, define one of three outcomes: agent resolves independently, agent escalates to team lead, agent transfers to an internal queue. For each internal queue, define what information must be in the transfer note and who the named contact is. This investment pays back the moment the first ambiguous case hits the queue.

Measure root cause, not just volume. First response time is easy to track but it's a proxy. The metrics that tell you whether the relationship is working are: first-contact resolution rate, escalation rate trend, DSAT broken down by agent-caused vs. product-caused, and case age distribution. When targets are missed, the conversation should be about root cause, not blame.

Why it matters and next steps

Top-notch support for payments platforms requires a blended approach using AI workflows that operate correctly, well-training human agents and an in-house escalation team to handle sensitive, hard-to-reverse decisions. All of this matters because with payment businesses:

- Response time is the product

- 24/7 coverage is the standard

- CSAT above 4.4/5 is hard but necessary

If you’re interested in learning more about payments support, schedule a quick chat here.

Get started with Influx

Influx was established in 2013 & has been trusted by 750+ brands globally, ranging from startup to scale.

Influx builds 24/7, near-shore global customer support teams. We provide fully managed, flexible & high-performance agents. Our services range from eCommerce support, tech support, sales support, AI Management, Enterprise solutions and more to give you the customer assistance you need to prioritize other responsibilities and continue scaling your business.

Make your support operations fast, flexible, and ready for anything with experienced, 24/7 support teams working on demand. See how brands work with Influx to deliver exceptional customer support or get a quote now.

Read these next

Or read our client testimonials or case studies